Transforming banking and capital markets

Howard Bush is a Principal, Banking & Capital Markets Lead in the Azure Cloud Industry Experiences team at Microsoft. As a practitioner of the “art of the possible,” Howard is a 25+ year banker wrapped in IT clothing impacting the Banking & Capital Markets Industry by building bridges to cloud adoption. Below, Howard provides insights on Open Banking and the global API Ecosystem.

The Road to Transformation

There has never been a better time to embrace digital transformation and innovation in Banking. Unfortunately, many global banks are being caught off guard by disruptive fintech innovation and swift moving regulatory requirements. On the road to that transformation, banks will have to quickly define the new value chains that will drive market share and growth in revenue.

As an accelerant to this banking innovation, there are two regulatory requirements coming out of the European Union (EU) where banks have to expose account information and service payments to/from Third Parties: The Second Payment Services Directive (PSD2) and The United Kingdom (UK) Competition and Markets Authority (CMA) Open Banking initiative.

In a nutshell, the regulatory directives are requiring banks to open up their backend systems (aka Open Banking or Banking as a Platform) via Application Programming Interfaces (APIs) to FinTechs and other banks. PSD2 and Open Banking are kick-starting the financial services revolution that will connect consumers, third party applications and banks in new ways using new business models.

Progressive Banks Have a Leg Up

Many banks are only beginning to take action on these regulations despite its massive repercussions it will have on their business. However, progressive organisations that embrace regulation and transform will be the winners. While banks in Europe must open up because of regulation, leading banks around the world are following closely and not waiting for the regulators. They are starting to provide API-based access to services to others. And some banks are pursuing a “marketplace banking” strategy, seeking to position themselves as a banking platform in the middle, on top of which third parties can build a myriad of discrete services.

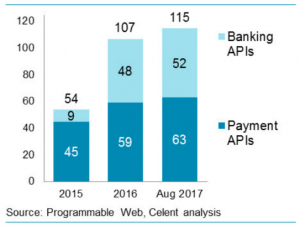

According to ProgrammableWeb.com’s global API directory, banks and fintech firms published more than 275 new payment and banking APIs in the past 2 ½ years.

Banking APIs or Banking as a Platform offers a gateway to an interesting ecosystem of trusted partners that will improve the customer experience, increase collaboration, speed up time to innovation, measure business impact, predict needs, devise new business models, new value chains and innovative products that customers need.

With greater accessibility to banking products and services, new market entrants will make it critical for banks to consider new approaches to empower employees, engage customers, optimize operations and transform products to stay competitive.

The Inflection Point and Microsoft’s Point of View

The key question banks need to think about is How will banks’ participate in a broader API economy?

Banks will likely not own the end-to-end value change as they will bring Third Party Providers (TPPs) into their ecosystem. Banking business models will transform to an open ecosystem of partnerships and new un-imagined capabilities. The new era for banking will lead for new opportunities and challenges not seen before. And the role of Banking will be redefined:

- Incumbents may be relegated to the role of pure component/product supplier and be subject to fierce price competition and limited grip on the customer experience, while being saddled with existing risk and capital requirements

- Incumbents will need to make some stark choices on how they wish to position themselves to capture future value

- Incumbents can develop their own aggregation and platform capabilities: for example, ING has launched the bank-agnostic Yolt personal financial management app in the UK

- Others may decide to retreat from the edge altogether and instead focus on becoming hyper efficient, user-friendly product suppliers – aiming to integrate into as many alternative digital sales outlets as possible

We feel marketplaces and the sharing economy are inevitable and those newly formed partnerships can pair the experience of banks with the agility of FinTechs to a win-win scenario by creating agility and collaboration needed as a key to success. Banks can turn regulation into Digital Transformation opportunity to leapfrog competition based on open and collaborative new business models to bring new value to their customers – new value chains will be formed.

To continue the dialogue on this fascinating topic and how Microsoft is driving the API economy through its Azure cloud platform, feel free to reach out to me on:

Twitter @HowardBush2 or Linkedin.

Howard Bush, Principal, Banking and Capital Markets Lead for Azure Engineering at Microsoft.

Find out more by downloading The Future Banking Ecosystem white paper